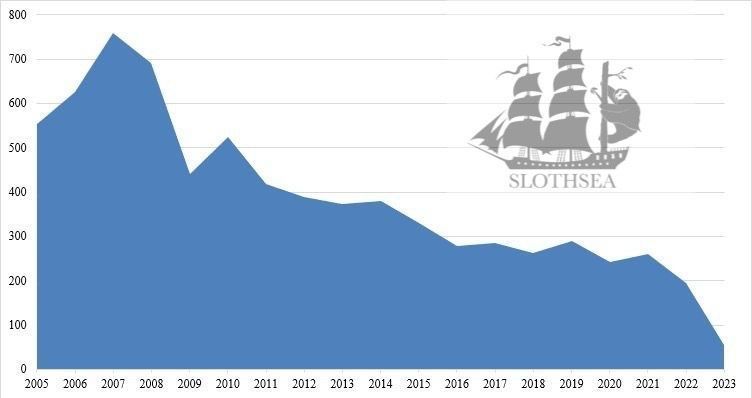

Is interesting to note how the global orderbook is decreasing in the last 20 years. If it wasn’t for the heavy push of the container sector in the 2020/21 that is now suffering such overcapacity, the below chart would show a drop even bigger. The new environmental rules imposed by IMO and the uncertainties of market, as the diagram shows, have carried to a vertiginous descent of the total number of yards engaged in new constructions. In some sectors as the Dry Bulk, moreover, the age of the ships will involve a further decrease of the fleet, determining perhaps situations of bullish market.

What should we expect?