The crisis triggered by the Houthi movement within the Red Sea since mid-November is generating multiple difficulties for shipping and the global logistics chain in general.

Shipowners and/or charterers, in fact, have found themselves having to choose between going through the Suez Canal, with a greater exposure to the risk of being targets of Houthi attacks, or circumnavigating the Cape of Good Hope, with a consequent increase in costs (for example bunker costs) and a longer sailing time estimated at ten days.

As of today, most ships are completing their circumnavigation of the African continent, and this has major repercussions on downstream players in the logistics chain such as terminal operators, receivers of goods and finally the end consumers of the product (in January there was a 38% drop compared to December 2023 for container ships).

In fact, the passage through the Cape of Good Hope generates a considerable reduction in maritime traffic within the Mediterranean Sea basin (with a diversion of this towards the so-called ‘Northern Range’) and a consequent decrease of ‘touches’ in the main ports such as Barcelona, Athens and Genoa.

On the other hand, a common discourse can be made regarding the receivers and final consumers of the product. Both subjects are strongly penalised in two respects: the first is that linked to the delay in the delivery of goods (with strong repercussions on the logistics chain, just think of semi-processed goods and raw materials from Asian countries) and the second, no less important, is the item linked to the costs that are directly passed on to these two categories, especially that of the final consumers.

What about marine insurance?

As one might expect, we are facing a very complex historical moment for maritime insurance, especially for those related to so-called war risks.

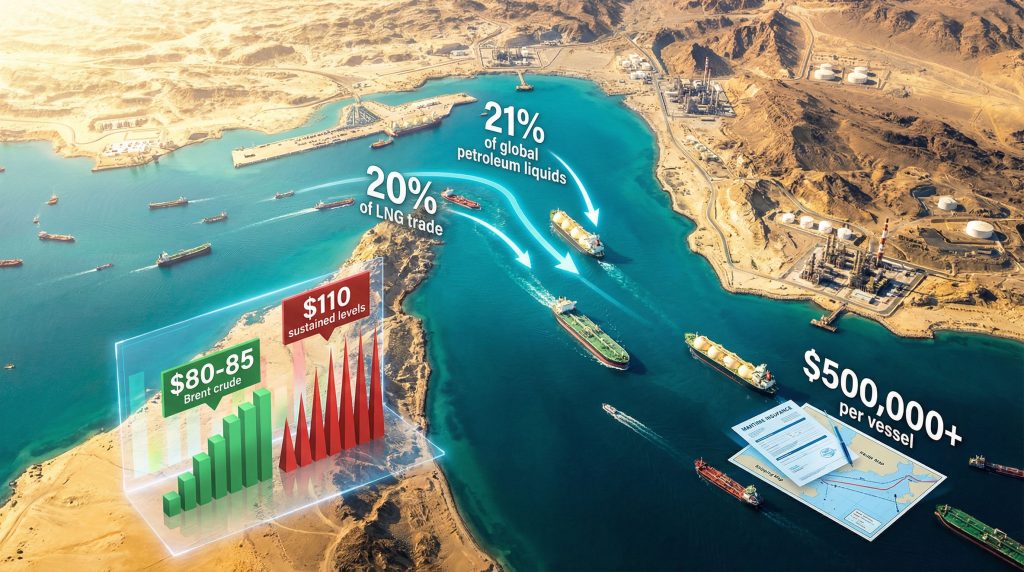

If in 2022 we had to deal with the problem of shipping within the Black Sea (with rates currently fluctuating constantly within a range between 0.90% and 1.25% of the ship’s value and with 24/7 validity), today the main problem is related to the exponential increase of the war premium for the Suez Canal area (Gulf of Aden).

In the space of just a few weeks, the shipping market, due to the increasingly frequent Houthi attacks and increasingly unclear criteria (from ships linked to Israel to those flying the British and US flags), was faced with both a rise in war premiums and a tightening of the conditions of cover (time validity subject to 24 hours).

The insurance market, predominantly the London market, moved decisively in one direction (with a few exceptions): adopting a rate hike from 0.0100% to peaks of 0.7000% – 0.7500% of the value of the ship, with a reduction even of No Claim Bonus that somehow generated a less heavy impact from a monetary point of view. This is equivalent to hundreds of thousands of dollars if we consider, for example, a ship with a value between 80 – 100 million dollars.

Faced with this scenario, most people would (also rightly) think of an enrichment of marine insurance companies; however, we could argue that we are facing a contradiction. The huge rate increases applied by the marine insurance market have effectively discouraged passage through the Suez Canal (which generates a time saving but still does not guarantee the safety of the seafarers and the ship even if insured), leading to the decision of ship owners and charterers to circumnavigate Africa with increased costs but at the same time with a higher vessel fill rate (reduction in the supply of transport) and a general increase in freight rates.

The next few weeks will be crucial to understand whether we will be faced with an ‘exceptional’ situation or one that we will be able to describe as somewhat structural.

#RedSea #Houthi #Shipping #Market #Marine #Insurance #Slothsea