The dry bulk market has entered 2026 on a noticeably weaker footing compared to the more optimistic tone seen toward the end of last year, with the BDI reaching about 2800 points at the beginning of last December. After averaging over 2000 points during Q4 2025, the Baltic Dry Index has corrected sharply over the past few weeks, sliding back into the 1,500–1,700 range. While these levels still represent a year-on-year improvement versus early 2025, when the index was hovering closer to 1,000 points, reaching minimum around 700 points, the pace of the recent decline has weighed heavily on sentiment. Seasonal softness, combined with limited Chinese buying interest since mid-December, has quickly erased much of the momentum built in the final months of last year.

On the demand side, the picture remains mixed and increasingly region-dependent. China continues to struggle to regain traction, with iron ore and coal imports expected to remain broadly flat compared to 2025, constrained by a still-fragile property sector and economic growth projected around 4.5%. While volumes have not collapsed, there is little evidence of a meaningful rebound. India, on the other hand, remains a clear bright spot, with dry bulk import growth estimated in the 4–6% range, supported by strong demand for thermal coal, iron ore, fertilizers and agricultural commodities. Elsewhere in Asia, minor bulks and industrial metals linked to infrastructure and energy-transition projects are providing some support, particularly for mid-sized segments, although not enough to fully offset weakness in the larger trades.

Supply fundamentals continue to be the market’s main headwind.

The global dry bulk orderbook/existing capacity ratio has increased compared past year and now accounts for roughly 14%, and despite an increase in demolition activity during 2025, deliveries continue to outpace removals. As a result, fleet capacity at the start of 2026 is estimated to be around 2% higher year-on-year, keeping utilization under pressure across most segments. At the same time, environmental regulations are increasingly shaping trading behavior. Costs related to EU ETS exposure and tighter IMO CII requirements are becoming more visible in daily operations, widening the gap between modern eco vessels and older tonnage and influencing charterers’ vessel selection.

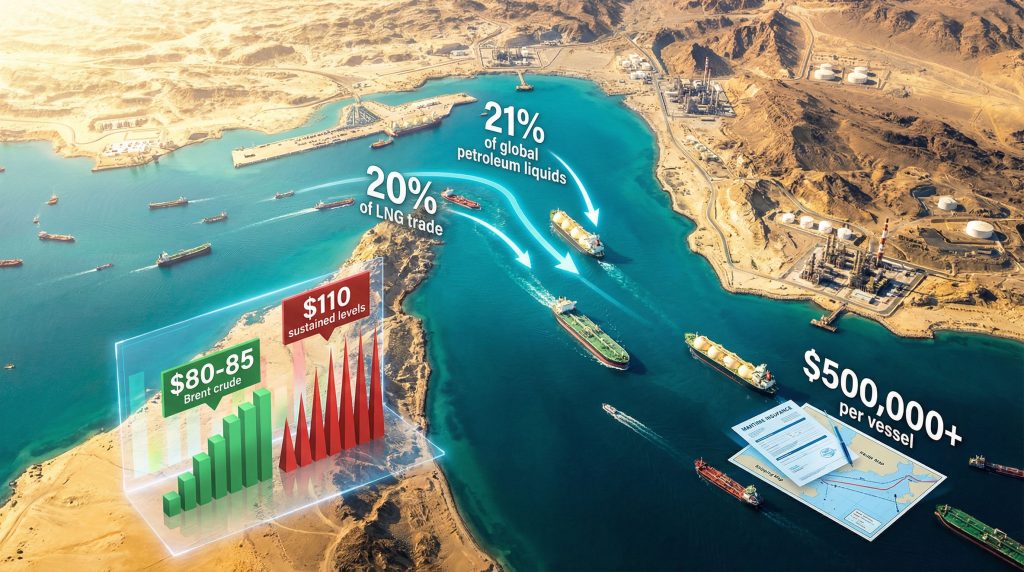

Beyond pure market fundamentals, geopolitics is adding another layer of uncertainty. Rising tensions involving Iran may increase risk premiums and insurance costs in the Middle East, particularly around the Strait of Hormuz, while ongoing instability of the Blond self-crowned King continues to affect trade flows all over the world. These factors have not materially reduced global dry bulk volumes, but they are contributing to higher volatility and a more cautious approach among market participants.

Overall, while early 2026 still looks slightly better than the same period last year in year-on-year terms, the sharp pullback from the stronger conditions seen in late 2025 serves as a reminder that the market remains fragile, highly seasonal, and sensitive to both supply growth and external shocks.